How BNPL Approves You in Seconds Using India's Financial Data Highway

Instant BNPL is not magic underwriting. It is a low-latency distributed system that fans out across bureau, consent-based financial data, fraud, and device signals on India's digital rails.

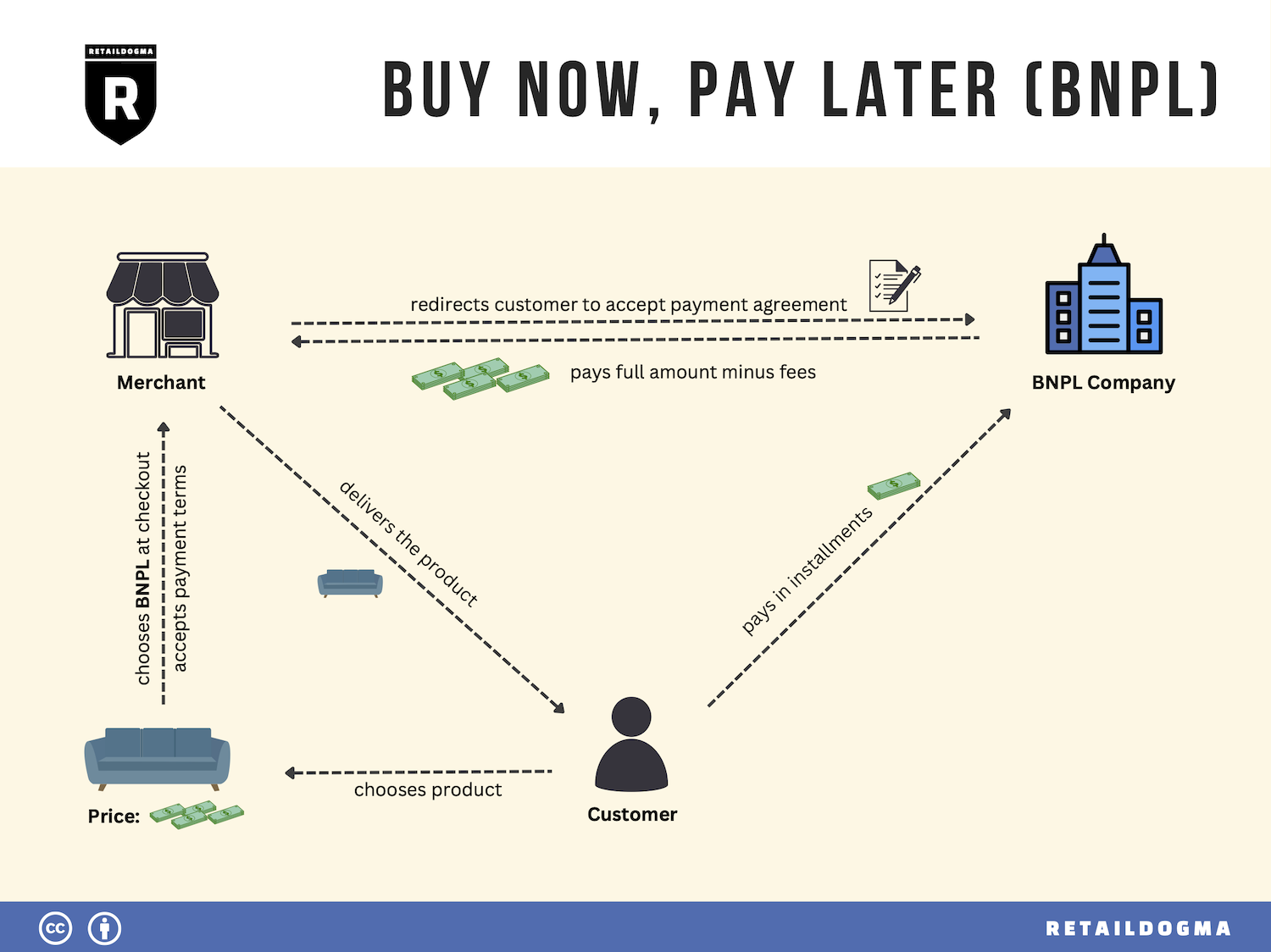

The Hook

What Instant Approval Actually Means

capture the application

verify basic identity and eligibility signals

fetch risk data from multiple sources

combine those signals into a consistent feature set

calculate a risk score

apply lender policy

return an approve, reject, or manual review outcome

The speed comes from two things:

- better data availability

- parallel system design

Without those two, the flow becomes slow very quickly.

Why India Is a Good Environment for This Architecture

digital identity-linked onboarding

soft bureau access

consent-driven financial data sharing

mobile-native user behavior signals

bank-linked verification and repayment rails

The most important design shift is this: instead of asking the user to upload proof and waiting for humans or OCR pipelines to interpret it, the lender tries to fetch machine-readable data through consented APIs and standardized rails.

That dramatically changes system design.

The Old Lending Flow vs the New BNPL Flow

upload documents

wait for parsing

wait for manual review

call the customer

re-check details

decide later

That flow is slow because every step depends on the previous one.

New flow. The BNPL mindset is signal-first:

capture a small amount of user input

fan out to many systems in parallel

build a risk profile in real time

make a bounded decision fast

That is why these systems feel instant. They are not skipping underwriting. They are compressing it into a tightly engineered backend workflow.

The Core Architecture Pattern

the app sends a small application payload

the decision engine validates it

the backend launches multiple risk checks in parallel

each risk service returns one part of the picture

the orchestration layer combines those parts into one feature vector

a scoring model estimates risk

a rules engine applies business policy

the system stores the decision and trace

the app receives the result

This is a classic fan-out and fan-in system: fan-out to gather signals, fan-in to produce one credit decision.